Greek crisis: global implications

10 March 2010

Jame Medway

This article first appeared on Counterfire.

The crisis in Greece continues, with a government, elected last October on a promise to increase public spending pushing through massive cuts; strikes, protests, and riots across the country; and the stability of the entire European Union threatened.

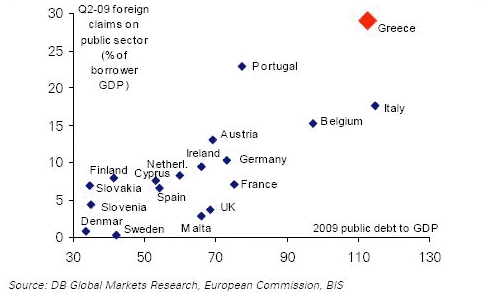

After years of exploiting its membership of the Euro for cheap loans, the Greek government’s levels of borrowing started to alarm lenders late last year. Greece national debt is now up to 160 per cent of its GDP, and the interest payments alone account for 5 per cent of its national output.

Major financial institutions fear that, with Greece in recession, this volume of debt and interest payments are unsustainable. A serious worry has developed that Greece may default on its debt – declare itself unable to repay, leaving lenders with gaping holes in their own finances. The cost of insuring Greek government debt against default increased by more than ten times in the few months before Christmas, as the financial markets realized that default was a serious prospect.

In response, the Greek ruling class is attempting to ram through an ‘austerity package’ of devastating cuts in public spending, including a public sector pay freeze, and sharp rises in taxation. This, it is hoped, will appease Greece’s many creditors. In other words, ordinary Greeks are being asked to make sacrifices to keep big finance happy.

But this is not just about Greece. Financial turmoil there provoked consternation and near-panic throughout the EU.

Two, related, terrors can give central bankers across Europe sleepless nights.

1: The risk of contagion

The first is ‘contagion’: financial instability spreading from one economy to the next, with country after country pulled into the maelstrom.

By itself, the Greek economy represents just 3 per cent of all the Euro GDP. But because financial markets tie economies together with debt, a financial crisis there has the potential to spread.

Other Euro economies are exposed to Greek upsets through the substantial investments various European financial institutions now hold there. French investors are the biggest, holding $58bn worth of Greek debt at the end of 2008 (on the IMF’s most recent figures), with German investors next on $32.3bn.

UK holdings are more modest, but still very substantial, covering $14.4bn worth of loans. Around a third of Greek government debt, meanwhile, is held by Greek investors. All will take a hit from substantial fiscal turmoil in Greece. And all the big exposures are in Europe.

Graph: Foreign bank holdings of European government debt

Greece remains the biggest single risk. Revisions to the public debt figures have rattled markets, while the deep spending cuts offered in sacrifice by the newly-elected PASOK government have not entirely calmed the jangled nerves of big finance.

If the banks and the institutional investors pull out of Greece, they can spread financial instability elsewhere – with speculators adding to the chaos, moving colossal volumes of hot money at fantastic speed across national borders. The whole Eurozone – potentially even the Euro project itself – could suddenly appear unstable. The dangers are sufficiently great that EU governments have started talking up restrictions and bans on some of the financial devices used by speculators.

2: The dangers of political instability

The last decade has been generous to the Euro. A benign economic environment, floating atop a giant property-and-finance bubble, kept the show on the road. Those days are long gone. A fundamental tension within the whole project has broken open: the failure of Europe’s ruling classes to deliver political union, alongside the single currency. Euro countries now all use the same notes and coins. But they maintain different governments with different budget plans. The Euro’s weak rules do not prevent these different governments spending and borrowing almost as they wish.

That is the second nightmare for the major European powers. There is no guarantee a bailout will work, with more and more cash being required to stem turmoil. And bailing out Greece may send a signal to other, smaller economies that they, too, will get bailed out. Because individual countries’ budgets cannot be enforced at the European level, they may be tempted to avoid austerity measures and hope for a bailout. The prospect of substantial future payouts could by itself cause financial markets to turn against the Euro.

It’s a dilemma for other European powers. Either course of action creates further problems. So there is no clear strategy to deal with the crisis. Sarkozy’s government has favoured a simple bailout, arguing that this will contain the crisis and that future costs will be limited. Angela Merkel in Germany, however, has so far firmly blocked the payment of any funds. Negotiations have produced a fudge, with European institutions providing oversight of the Greek government’s austerity package, but no additional assistance.

And some of the wiser Keynesians around the ruling class, Joseph Stiglitz amongst them, are pointing out the dangers of massive spending cuts and attacks on wages in reinforcing the recession in Greece, dragging the economy further down – and then potentially producing another debt and currency crisis.

As the SOAS Research on Money and Finance group will argue in a report due next week, Germany’s weak economic growth and stifled domestic demand has steadily undermined the Eurozone. It may be the heart of the European economy, but it is increasingly frail. The CDU-led government there remains committed to a tight spending policy, and domestic pressures alone may prevent Germany offering any assistance.

For now, the situation has been somewhat eased. A semblance of unity has been created around the EU’s rather empty promises, and that – at least – is better for the European ruling class than open squabbling. The apparent backing of Barack Obama for the Greek government has also eased the situation. EU bigwigs like former Commissioner Romano Prodi are claiming that the crisis is “completely over”.

But the markets are not wholly reassured by it all. The cost of insuring Greek debt against default has declined, as investors believe this is now less of a risk. But it is still more than double the cost it was in November. Spanish and Portugese default insurance costs also remain very high.

There is now immense pressure on the Papendreou government, from across Europe, to deliver the package of spending cuts his government have signed up to. Perceived failure here, or indeed simply a fresh outbreak of panic on the financial markets, would shatter this uneasy calm.

The financial vacuum

Meanwhile, the International Monetary Fund, a Washington-based institution battered, over the last decade or more, by failed interventions and the anti-capitalist movement, is sniffing around Greece. The IMF was established to provide emergency funding to economies perceived to be in serious financial difficulties.

These loans come at a heavy price, however. Tough conditions are attached, carefully calibrated to pummel a failing economy into a shape more appealing to the finance markets. Shrinking public services, clamping down on wage growth, and allowing capital to flow freely in and out of the country are all typical measures.

IMF money has been used during this crisis to bail out some smaller economies in eastern Europe. Bailing out an EU member would, however, be a different story. In theory, at least, EU economies – and the European institutions, like the European Central Bank – should be able to look after themselves. For Greece to call in the IMF would be a major political defeat for the European project, seriously undermining the Euro.

Yet the IMF itself is nowhere near as powerful as it once was. Its role as effectively “lender of last resort” to stricken economies has been challenged by the rise of regional funding schemes – the Chian Mai Initiative in East Asia, and the Banco del Sur for Latin America. Both, potentially, undermine the IMF’s ability to intervene as it – or, rather, Washington – sees fit in a crisis. And behind the IMF’s slide from grace lies the steady decline of US economic power in the world.

Angela Merkel and other EU leaders now back the creation of a “European Monetary Fund”. But it’s not clear that Europe’s bickering ruling classes could establish a sufficiently robust institution amongst themselves. The European Central Bank itself remains strongly opposed to the initiative, fearing it would merely encourage further financial profligacy. Such disagreements may make the EMF a rather toothless body.

Without strong institutional anchors, backed up by a powerful state – as the US was once able to provide – the world financial system is at increasing risk of instability. Already, the first signs of competitive currency devaluation, as between the US and China, are appearing. “Beggar-thy-neighbour” policies like this, with each economy attempting to race every other economy to the bottom, helped exacerbate the Great Depression of the 1920s. It took the overwhelming dominance of the US, after 1945, to re-establish any sort of monetary and financial stability across the Western world.

This crisis has revealed that the EU can barely provide that level of stability to its own members, let alone globally. Brave talk of the Euro replacing the dollar as the international currency of choice, widespread a few years ago, now looks empty. Instead, a growing vacuum is appearing at the heart of the world financial system, with no currency or state powerful enough to fill it.

The need for political resistance

The deciding factor, however, will be political. Either the Greek government can keep the markets reasonably sweet, holding firm to bigger and bigger attacks public services and wages; or the markets will be unconvinced, spreading chaos across Europe.

The signs, for capital, are not entirely promising. European officials are alarmed by the slow planned pace of Greek spending cuts, fearing that this will not be enough to appease finance.

And the cuts are meeting solid resistance. A general strike is planned for Thursday this week – the third this year. Sacked employees of Olympia Airways have occupied the Ministry of Finance, and government printers have staged a sit-in at their workplace. Police have attempted to break up crowds of protestors with tear gas.

Opinion polls that once favoured Papandreou’s austerity measures have started to shift. Public opinion is now on a knife-edge, with 46 per cent supporting the measures and 47 percent against. The resistance the cuts have met already, and the very real impact they will have on living standards, are turning the tide on the government.

But without a broad, political response on the left to economic crisis, the dominant story becomes the one the various neoliberal governments want: of “profligate” public services needing to be cut to pay for hard-up bankers.

The Greek working class and protest movements have a solid recent history of struggle – so much so that, after days of rioting there following a police shooting in 2008, Nicholas Sarkozy was apparently moved to remark that he did not want “another May ‘68” in Europe. Any austerity programme will run into this well-trained opposition. Serious opposition in Greece, meanwhile, could open the path for resistance across Europe. Sarkozy’s worse fears could be realized.

The stakes are becoming very high. Either the government, and behind it, the EU itself, will be pushed back. Or the opposition will be broken – and, within living memory, Greece has suffered a military dictatorship. A determined ruling class will only be broken by a united, political opposition.

No comments:

Post a Comment

Comments